Umba

What’s the issue?

With a stricter approval target on the lending algorithm, many new and existing users were getting declined for loan applications. This lead to most new users dropping off shortly after the loan decline. I was tasked with finding a way to reduce this drop-off.

What was my impact?

40% increase in the # of users retained after loan decline.

Team

Product Designer

Product Manager

2 Engineer

Data Analyst

QA Analyst

Timeline

Week 1: Design

Week 2: Develop

Week 3: QA & Launch

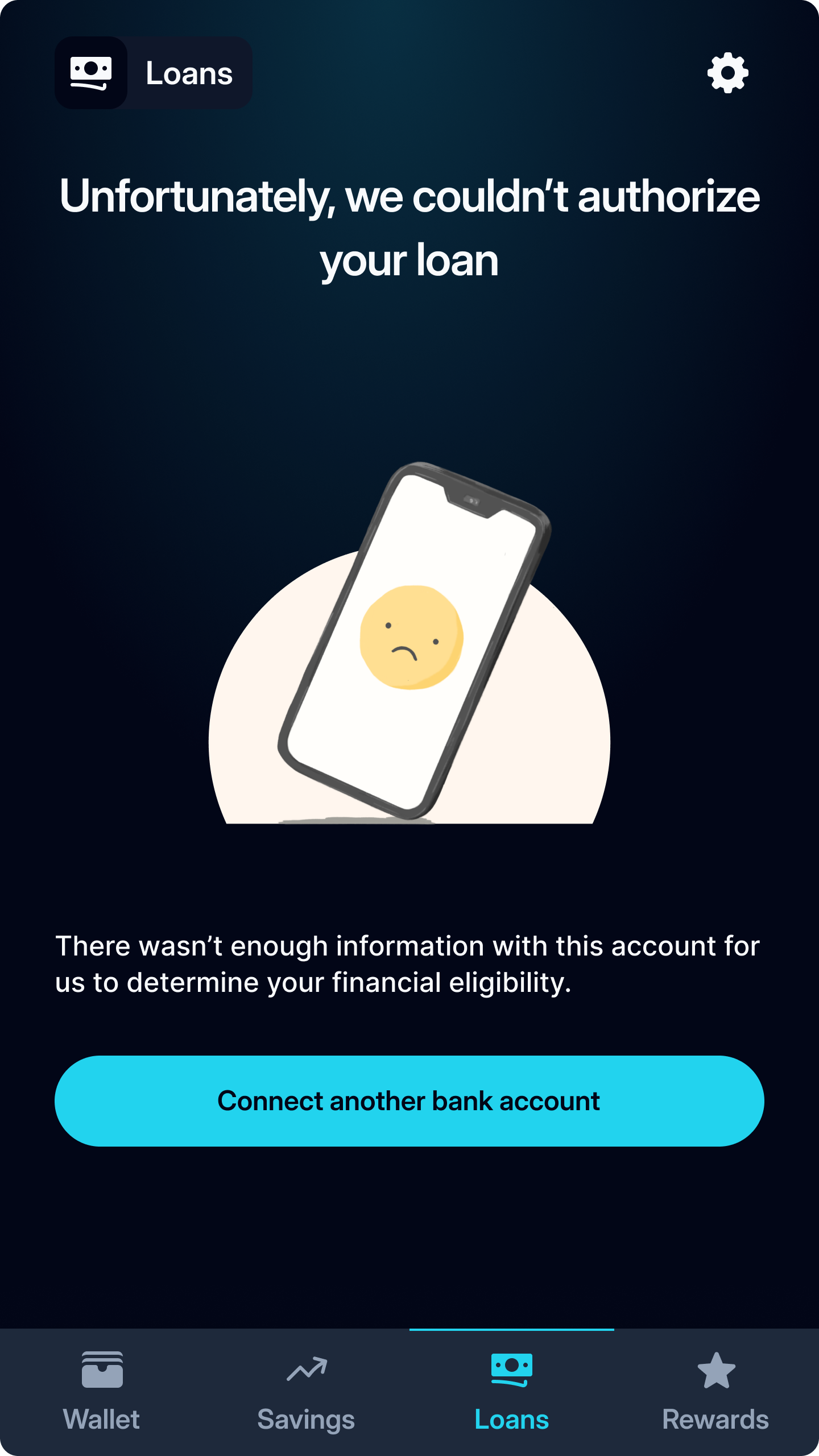

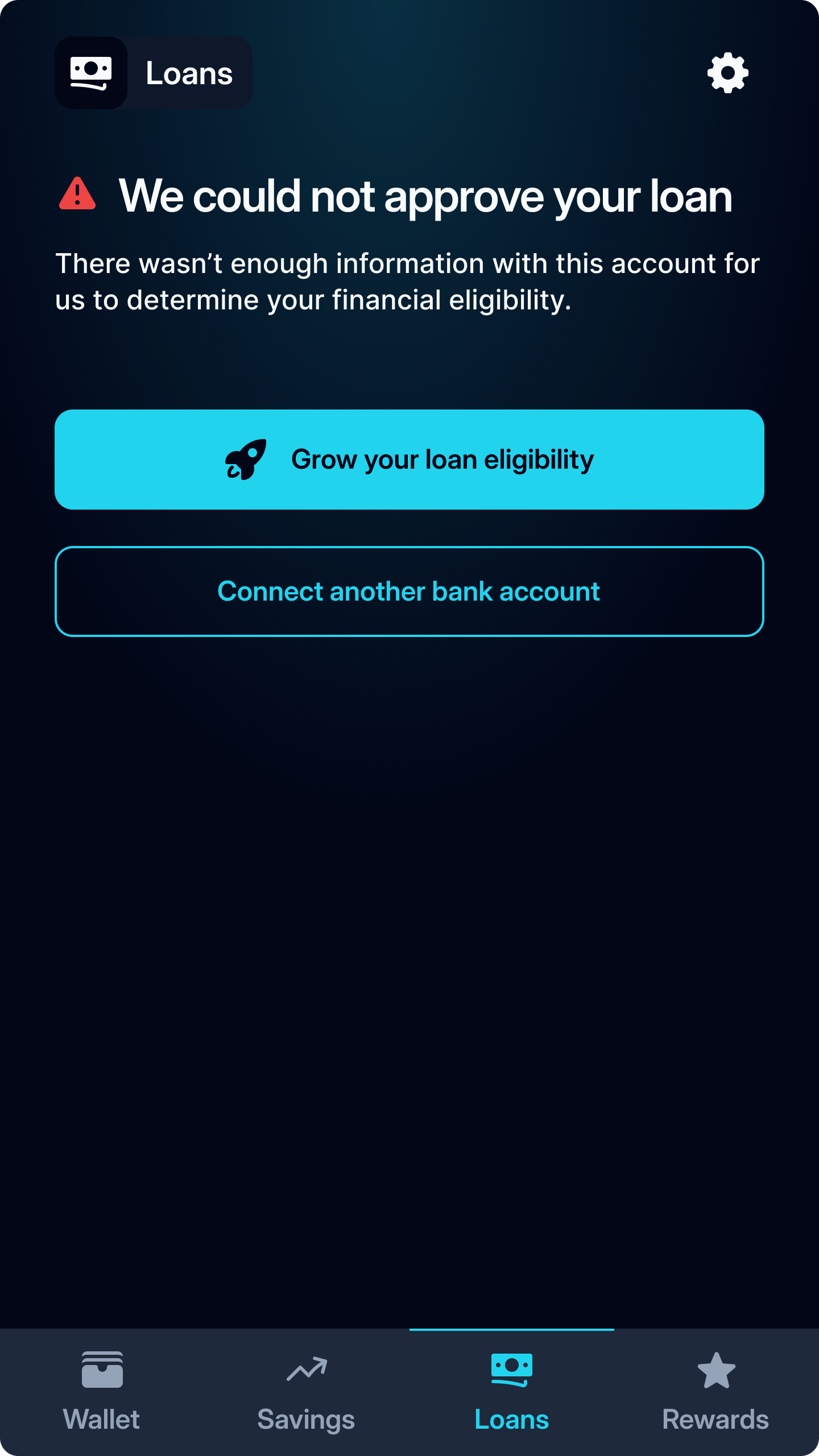

I got declined... Now what?

So why should I stay?

The current loan decline flow forces users out of the app, with little context on what they can do to become qualified for a loan.

What’s the negative impact?

We see 70% of users deleting the app after a loan decline.

What could be happening?

Graphic is frustrating to users

Users rarely have a second account

Unclear what to do to qualify

Creating alignment between the users, business, and product

Important to users

Have a clear path for how to qualify for a loan

% of users retained

Important to the business

Curbing risky loans through the ML based algorithm

% of loans defaulted

Important for the product

Build and keep trust with users through reliable service

# of loan decline support tickets

How did we get set these metrics?

Users voice there concerns in reviews, to customer support, and during interviews

The business metrics are set during leadership meetings to align with investors

Product works cross team to determine what is indicative of a good experience

Testing user motivations

What are people willing to do?

With a fake door test we were able to see what users were most inclined to interact with when if came to growing their loan eligibility.

What were the results?

We see 20% of users completed other feature flows such as bill pay & buying airtime.

What could be happening?

Users are interested in becoming eligible

Not all users engage with the same features

We need more incentive to retain more users

Looking at the data

Some surprises are good!

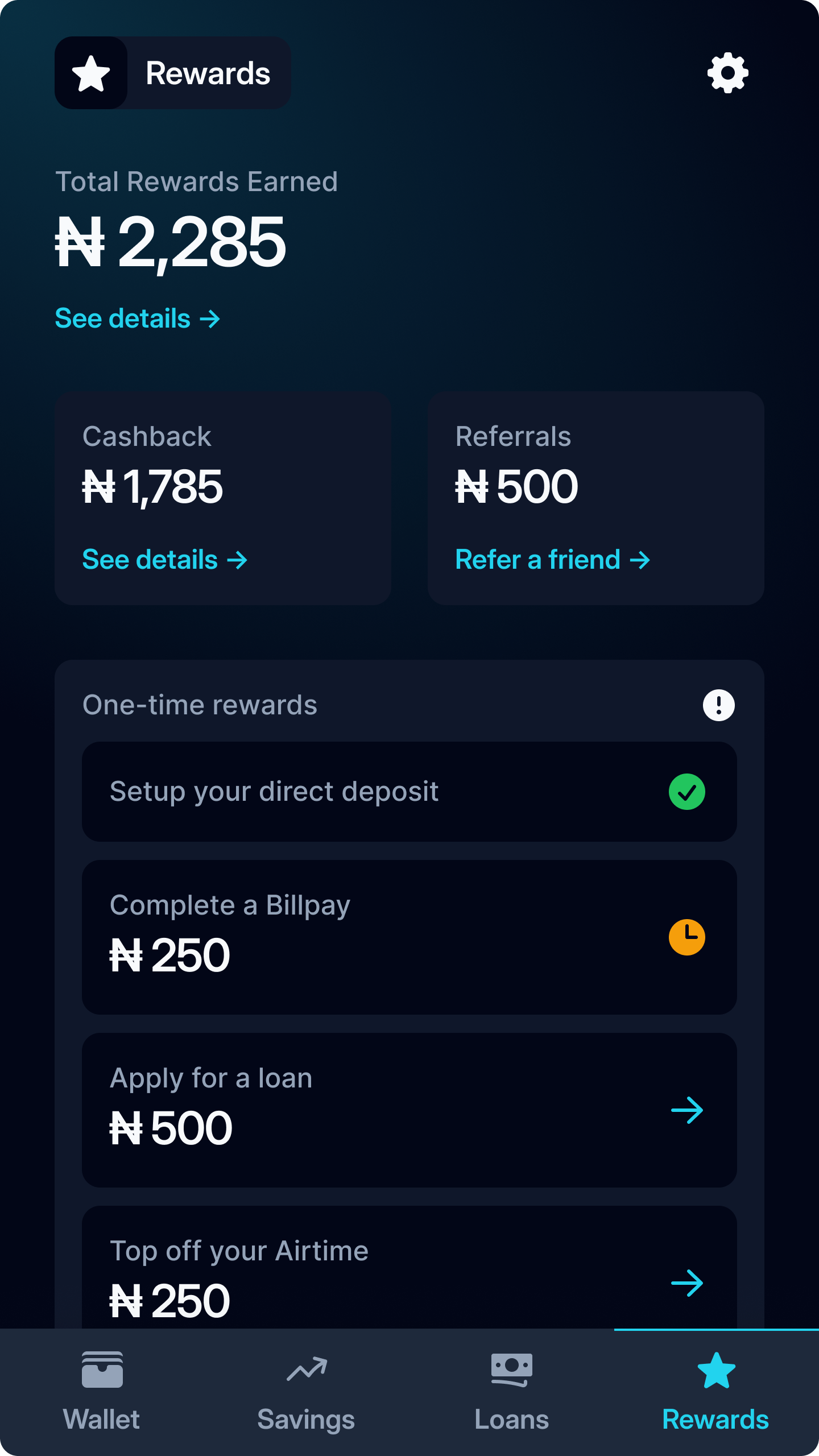

Our data analyst showed the team that more than half the users were clicking into the rewards tab after loan decline.

But we were dropping the ball

The current “rewards” tab was nothing more than analytics on most likely empty data. No wonder users deleted the app afterwards.

What’s the opportunity?

We have a clear user incentive

We can utilize organic movement

The rewards tab is a blank slate

Leveraging organic movement

Combining our learnings

We know users are open to trying other features to grow their loan eligibility. We also know users are organically moving to the rewards tab in hopes of some money.

Creating a symbiotic system

Using the incentive of monetary rewards, I developed a First Time User Experience that exposes users to all features within Umba.

What do we hope this accomplishes?

Creates user habits around banking features

Leaves the users with a positive experience

Give users a head start to grow eligibility

Halved losses for the month and planned for long term growth

Users impact

40% of users retained

Features like bill pay & airtime turned out to be sticky features

Business impact

<5% of loan defaulted

We set key levers that users can pull to affect our algorithm

Product impact

2 week ticket backlog cut to 1 day

CE & Product set shared metrics that aligned our teams

How did we launch & validate?

Released in stages of users by 10%, 30%, 100%

Worked with finance to set reward amounts relative to average acquisition & retention costs

Partnered with CE to get support ticket data and consistent reporting on ticket backlog

Next Case Study: Simi